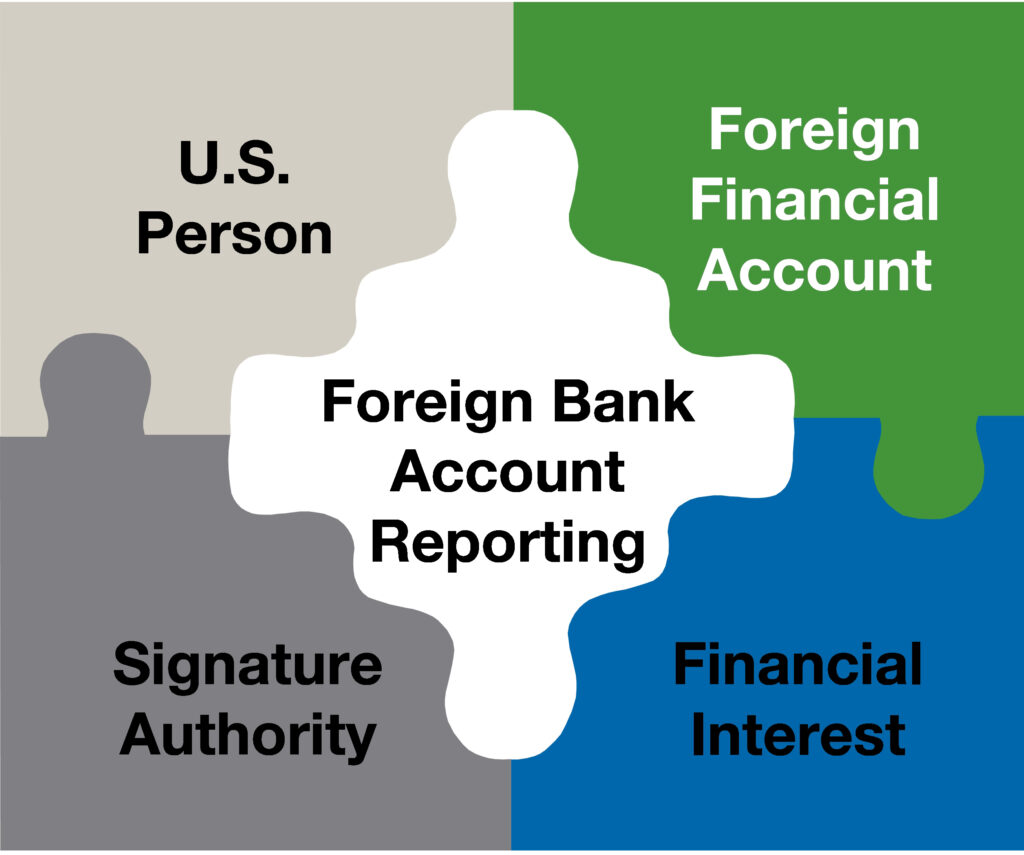

FBARs

FBARs

Willful FBAR Penalty Moving Towards a Strict Liability Standard

Assessment of the “willful” FBAR penalty Courts have sustained FBAR penalties by reference to case…

New Developments in The Willful Civil FBAR Penalty

Current Developments May Make It Easier For the IRS To Assess Penalties After Willfully Failing…

FBAR Enforcement: How and When the IRS Will Act?

How Does the IRS Enforce the FBAR? The Report of Foreign Bank and Financial Accounts,…

Secret Foreign Bank Accounts Are Not Secret Anymore…

Secret Foreign Bank Accounts Secret foreign bank accounts have been at the center of money…

FBAR Case on United States v. Carl Zwerner settled for $1.8 Million

FBAR Case: United States vs. Carl Zwerner is settled for $1.8 Million The United States…